Log in

Log in Free Trial

Free Trial karina

karina  Updated on June 20, 2026

Updated on June 20, 2026  27433 views

27433 views  27

27

Saving for a down payment and qualifying for a mortgage can take years. For many buyers, that makes homeownership feel out of reach. Lease-to-own and lease purchase agreements offer another path by allowing you to move into a home now and buy it later.

These agreements can help buyers who need more time to improve their credit, save money, or qualify for a home loan. However, many people still have questions about how they work, what they cost, and what happens if they decide not to buy the property.

This guide explains the difference between lease-to-own and lease purchase agreements, how each housing agreement works, and what buyers should know before signing a contract. You will also learn the benefits, risks, and key terms that can affect your future purchase.

Whether you are considering rent-to-own homes or reviewing a lease-to-own contract in 2026, understanding the details can help you make a more informed decision.

👉 Explore innovative paths to homeownership! Simplify lease-to-own agreements with RentPost’s powerful tools. Start your free trial now.

Key Takeaways: Lease to Own vs Lease Purchase

- Lease to own means you rent now and decide later if you want to buy. It gives flexibility and low risk.

- Lease purchase agreement means you commit to buy from the start. It offers a clear path but comes with a higher risk.

- Lease-to-own works best if you need time to improve your credit, save money, or test the home before buying.

- Lease purchase works best if you are sure about the property and just need time to complete the loan approval.

- Rent credits may apply in both, but they are more common in lease-to-own deals. Always check the contract terms.

- The biggest difference is flexibility vs commitment. One gives you a choice, the other requires you to follow through.

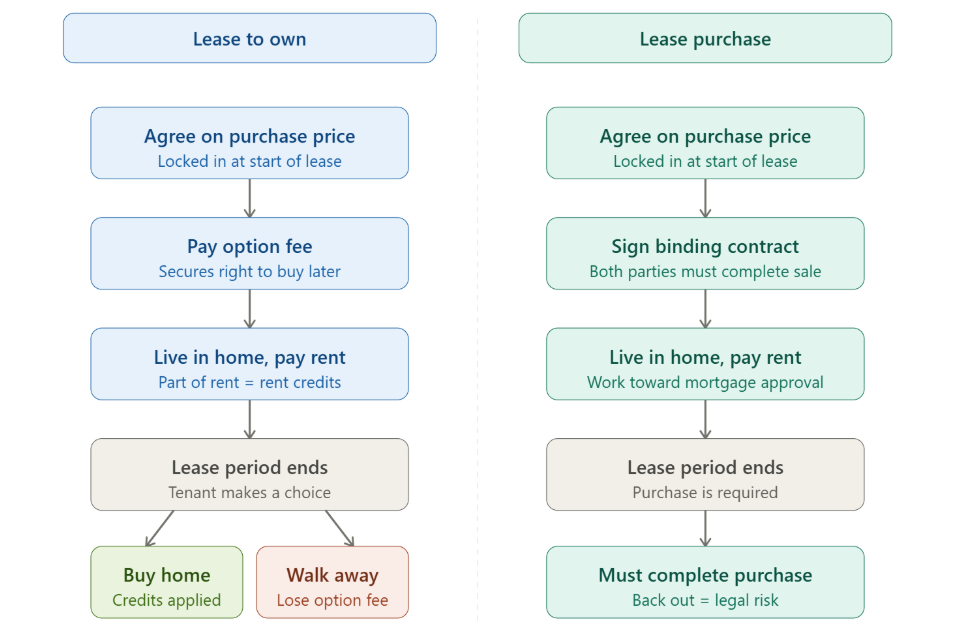

What’s the difference between Lease to Own and Lease Purchase agreements?

Both lease-to-own and lease purchase agreements help tenants move toward buying a home while renting, but the terms and obligations differ significantly.

| Feature | Lease to Own Agreement | Lease Purchase Agreement |

| Buyer’s Obligation to Buy | Optional – the tenant can walk away | Mandatory – tenant must buy at the end of the lease |

| Seller’s Obligation to Sell | Required – seller must sell if the tenant chooses to buy | Required – seller must sell |

| Option Fee | Usually paid upfront; non-refundable | May or may not be required |

| Rent Credits | Often included; portion of rent goes toward down payment | Less common; varies by contract |

| Flexibility | High – suitable for uncertain buyers | Low – best for committed buyers |

| Legal Risk for Tenant | Low – no penalty for not buying | High – may lose payments or face breach of contract |

| Ideal For | Tenants building credit or saving for a down payment | Tenants who are mortgage-ready and want to lock in a home |

| Purchase Price Timing | Locked in at lease start | Locked in at lease start |

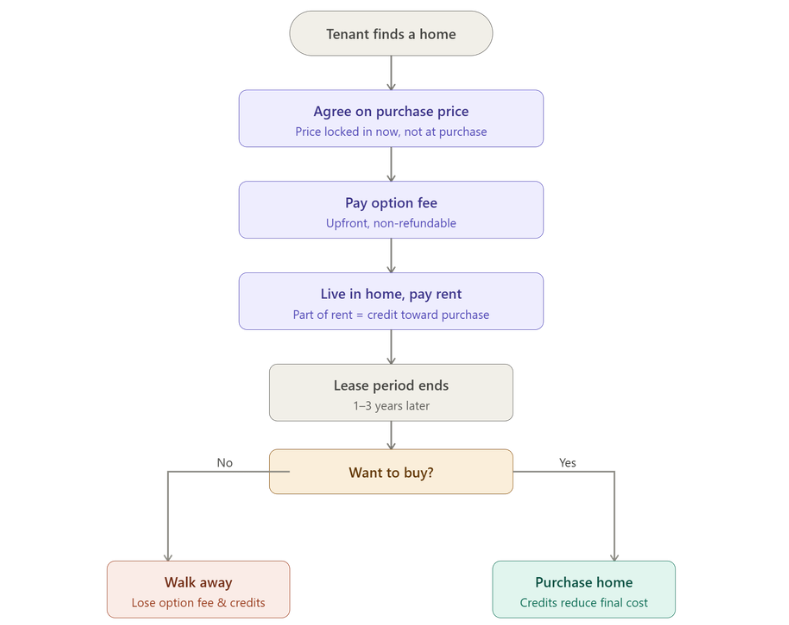

What is a Lease to Own Agreement?

A lease-to-own agreement is a rental setup where a tenant lives in a home with the option to buy it later at a fixed price. Many people also call this a rent-to-own agreement.

If you are wondering what does lease to own mean, it simply means you rent the home now and decide later if you want to purchase it.

This option works well for people who cannot qualify for a home loan today but plan to buy in the future. It gives them time to improve their finances while still moving closer to ownership.

How does lease-to-own work?

In a lease-to-own contract, the tenant pays an upfront fee to secure the right to buy the home later. This is often called an option fee.

- The buyer and seller agree on the price at the start

- The lease period usually lasts 1 to 3 years

- A part of the monthly rent may go toward the final price

- The tenant gets time to prepare for ownership

At the end of the lease, the tenant can choose to buy the home or walk away. This is why many people prefer this model when exploring rent-to-own homes. It gives flexibility without full commitment.

Why do people choose to lease to own?

A lease-to-own agreement gives tenants time and control. It helps them:

- Improve credit score

- Save money for a down payment

- Test the home and area before buying

This makes it a good option for buyers who are not fully ready but want to move toward ownership.

Pros of a Lease-to-Own Agreement

A lease-to-own agreement offers a balanced path for buyers who need time but still want to move toward ownership.

1. Greater flexibility: The biggest advantage is choice. The tenant has the option to buy, not a legal duty. If plans change or finances do not improve, they can walk away without legal consequences.

2. Gradual financial progress: In many lease-to-own contracts, a part of the rent goes toward the future purchase. This helps tenants build value over time instead of paying rent with no long-term return.

3. Protection from rising prices: The purchase price is fixed at the start. If the market goes up during the lease period, the tenant still buys at the lower agreed price. This can create instant value at the time of purchase.

4. Better decision making: Living in the home before buying gives real clarity. The tenant can assess the property, location, and lifestyle before making a final commitment.

Cons of a Lease-to-Own Agreement

While the model offers flexibility, it also comes with financial and practical risks.

1. Higher monthly cost: Most rent-to-own homes come with higher rent. The extra amount often covers future purchase benefits, but it still increases monthly expenses.

2. Upfront financial risk: The option fee is usually non-refundable. If the tenant decides not to buy or cannot proceed, this amount is lost.

3. Uncertain loan approval: Even after the lease period, the tenant must qualify for a mortgage. If they fail to secure financing, they lose both time and money invested in the deal.

4. Contract complexity: A lease-to-own agreement includes detailed terms about pricing, credits, and timelines. If not reviewed carefully, it can lead to confusion or unexpected outcomes later.

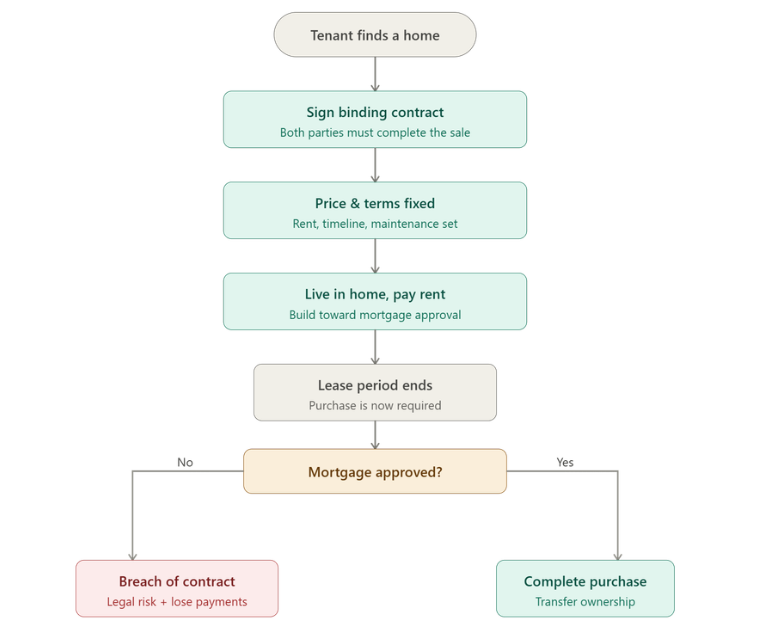

What is a Lease Purchase Agreement?

A lease purchase agreement is a legal contract where a tenant rents a property with a firm commitment to buy it at a fixed price after the lease ends. It means the buyer and seller agree from the start that the sale will happen later. This is not optional like a lease-to-own setup.

In this type of lease purchase contract, both sides have clear duties. The tenant must buy the property, and the owner must sell it under the agreed terms.

How does a lease purchase work?

At the start of the agreement:

- The purchase price is fixed

- The lease period is clearly defined

- Monthly rent and payment terms are set

- Roles for maintenance, taxes, and insurance are outlined

Some lease-to-purchase agreements may include rent credits. This means a part of the rent goes toward the final price. However, this is not always included and depends on the contract. This model suits buyers who are serious about ownership and want a structured path to secure the property.

Why do people choose a lease purchase agreement?

A lease purchase agreement gives buyers structure and commitment. It helps them:

- Secure the home they want early

- Lock in the purchase price in a rising market

- Get time to complete the loan approval

- Plan finances with a clear buying timeline

- Move forward with ownership without delay

This makes it a good option for buyers who are ready to buy but need a short gap before finalizing the purchase.

Pros of a Lease Purchase Agreement

A lease purchase agreement works well for buyers who are confident and ready to commit.

1. Clear ownership timeline: The agreement sets a direct path to ownership. There is no uncertainty about whether the sale will happen. This helps buyers plan their finances with more clarity.

2. Fixed purchase price: The price is locked at the beginning. If the market rises, the buyer gains by purchasing the property at a lower pre-agreed rate.

3. Structured financial progress: Some agreements include rent credits. This allows tenants to move closer to ownership while making regular payments, instead of starting from zero later.

Cons of a Lease Purchase Agreement

A lease purchase contract is stricter and comes with higher risk.

1. No exit flexibility: Unlike a lease with an option to buy, this agreement requires the tenant to complete the purchase. Backing out can lead to financial loss or legal issues.

2. Market risk: If property prices fall, the buyer still has to purchase at the agreed higher price. This can reduce the overall value of the deal.

3. Financing pressure: At the end of the lease, the buyer must secure a mortgage. If they fail to do so, they may lose rent credits, upfront payments, and the chance to own the property.

Lease to Own vs Lease Purchase: How does the option to buy differ?

The main difference between these two models is whether buying the home is optional or required.

In a lease-to-own agreement, the tenant gets the right to buy the home later, but there is no obligation. They pay an option fee to lock the price, and at the end of the lease, they can decide whether to move forward. If they choose not to buy, they can walk away without legal consequences, though they may lose the upfront fee and any rent credits.

In contrast, a lease purchase agreement is a firm commitment. The buyer agrees from the beginning to complete the purchase when the lease ends. All key terms are fixed early, and backing out is not easy. It can lead to financial loss or legal issues. This makes it better suited for buyers who are fully prepared to follow through.

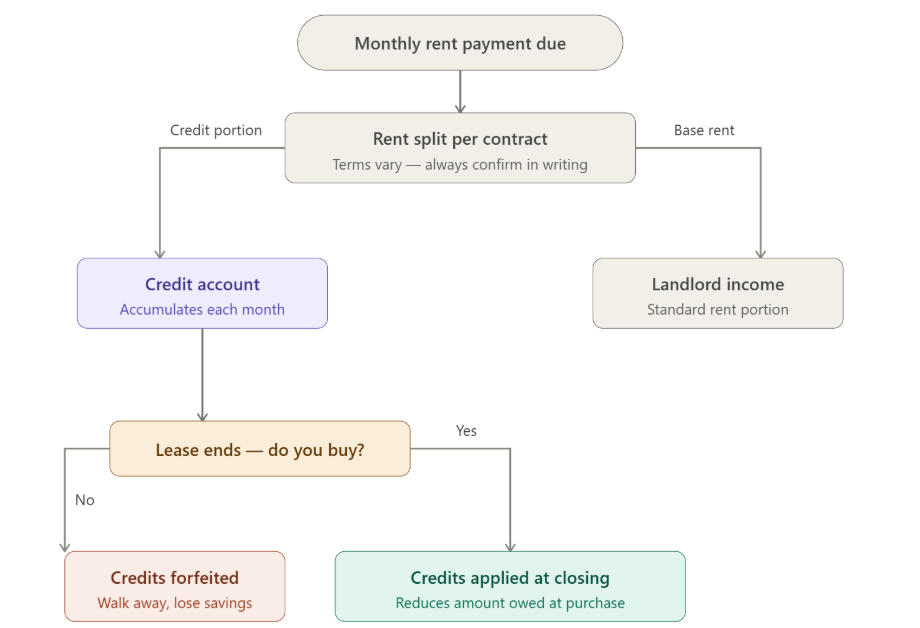

Lease to Own vs Lease Purchase: How do rent credits differ?

Rent credits decide how much of your monthly payment helps you move closer to ownership.

In a lease-to-own agreement, rent credits are often included.

- A part of the rent goes toward the final price

- This reduces the amount needed at the time of purchase

- It supports buyers who are still saving

This is why many rent-to-own homes attract buyers who want to build value step by step.

In a lease-to-purchase agreement, rent credits are not always included.

- The main focus is on completing the sale

- Rent may or may not contribute to the purchase

- Terms depend fully on the contract

Before signing any rent-to-own contract or lease purchase deal, always confirm how rent is treated.

Tip: Ask clearly if your monthly rent reduces the final purchase price. This can change your total cost in a big way.

Lease to Own vs Lease Purchase: Which offers more flexibility?

Flexibility is one of the biggest differences between these two options.

A lease-to-own contract offers more freedom.

- The buyer can choose whether to purchase

- There is no legal pressure to complete the deal

- It suits people who are still preparing financially

This makes it a strong option for those exploring lease-to-own homes or planning to buy later.

A lease purchase agreement is more strict.

- The buyer must complete the purchase

- Backing out can lead to financial and legal consequences

- It requires strong financial readiness

This model works best for buyers who are confident and ready to move forward without delay.

Note: Always review the terms of any lease purchase agreement or lease option deal carefully. If needed, take legal advice before signing.

Lease to Own Agreement: Benefits for Buyers and Owners

Benefits for the property owner

1. Attracts committed, long-term tenants: A lease-to-own agreement brings in tenants who plan to become owners. They usually take better care of the home, stay longer, and reduce day-to-day management effort.

2. Higher income with added security: Owners can earn an upfront option fee along with slightly higher monthly rent. This creates stronger and more predictable cash flow compared to standard rental setups.

3. Flexible exit and selling approach: This model allows owners to delay the sale while still earning income. It works well in uncertain markets where finding the right buyer may take time.

Benefits for the buyer or tenant

1. Time to prepare without pressure: A lease-to-own contract gives buyers time to improve credit, increase savings, and plan for a mortgage without rushing into a purchase.

2. Gradual financial progress: Many rent-to-own agreements include rent credits. This allows tenants to contribute toward the future purchase while continuing to live in the home.

3. Protection from price increases: The purchase price is fixed at the start. If property values rise, the buyer benefits by securing the home at an earlier price.

Lease Purchase Agreement: Benefits for Buyers and Owners

Benefits for the property owner

1. Clear commitment and reduced uncertainty: A lease purchase agreement ensures that the buyer intends to complete the purchase. This gives owners confidence and reduces deal risk.

2. Consistent income with a planned sale: Owners earn steady rent during the lease period and complete the sale later. This creates a balanced mix of short-term income and long-term return.

3. Stable tenancy and lower turnover: Since the tenant plans to buy, they are more likely to stay for the full term and maintain the property well. This lowers vacancy and replacement costs.

Benefits for the buyer or tenant

1. Secures the home early: A lease purchase contract allows buyers to lock in the property before finalizing the purchase. This reduces the risk of losing the home in a competitive market.

2. Clear timeline and financial direction: The agreement sets a fixed timeline for purchase. This helps buyers plan their loan approval, savings, and final payment with more clarity.

3. Early progress toward ownership: Some lease-to-purchase agreements offer rent credits. While not guaranteed, they can reduce the total amount needed at closing.

Lease to Own vs Lease Purchase Agreement: Which one is a good idea?

When is a Lease to Own Agreement a good idea?

A lease-to-own agreement works well for renters who need time and flexibility before committing to a home purchase.

- It’s a practical option for tenants with low credit scores who aren’t ready to qualify for a mortgage. The lease period allows time to strengthen financial standing while still moving toward homeownership.

- It benefits buyers looking to lock in a property at today’s price in a rising market. If home values increase during the lease, the pre-agreed purchase price can create instant equity.

- It suits individuals going through job transitions or relocation. The structure allows them to live in the home, explore the area, and delay full commitment or break the lease without legal risk if plans change.

When is a Lease Purchase Agreement a good idea?

A lease purchase agreement is better suited for buyers who are confident about ownership but need time to meet financing requirements.

- It helps tenants who are prepared to settle but need more time to meet mortgage qualification standards. The agreement ensures they don’t lose their home while improving their eligibility.

- It appeals to buyers who want to treat their monthly rent as a stepping stone toward the purchase. With some contracts offering rent credits, it’s a structured way to accumulate a future down payment.

- It’s a reliable path when the property owner is committed to selling to that specific tenant. This mutual agreement supports a stable, long-term transition into ownership without the uncertainty of backing out.

💡 Not sure which agreement is right for you, Lease to Own vs Lease Purchase?

Use this quick checklist to find out whether Lease to Own or Lease Purchase fits your situation best — in under 60 seconds.

📝 Should You Choose Lease to Own or Lease Purchase?

How RentPost helps Lease to Own vs Lease Purchase Management

Property management software like RentPost™ helps simplify and manage both lease-to-own agreements and lease purchase agreements. It reduces manual work and keeps everything organized.

1. Better communication and coordination

RentPost™ allows landlords and tenants to share updates, terms, and timelines in one place. Automated messages keep both sides informed, which reduces confusion and avoids missed details.

2. Faster and accurate documentation

Lease agreements include many legal and financial terms. RentPost™ provides ready templates and e-sign features, which help create, edit, and sign contracts quickly while reducing errors.

3. Clear financial tracking

The platform tracks rent payments, option fees, and any rent credits in real time. This helps both parties stay aligned on payments and avoids disputes later.

4. Automated reminders and deadlines

4. Automated reminders and deadlines

RentPost™ sends alerts for key dates like rent due, option deadlines, and purchase timelines. This ensures that both landlords and tenants stay on track and do not miss important steps.

Ultimately, Rentpost™ enhances the overall efficiency, transparency, and communication in the lease-to-own or lease purchase process. This creates a more organized and streamlined experience for all parties involved, making the transition from renting to homeownership a seamless undertaking.

FAQs

1. What is the difference between lease-to-own and lease purchase?

The key difference is commitment. A lease to own agreement gives you the option to buy, but you are not required to. A lease purchase agreement requires you to complete the purchase at the end of the lease. One offers flexibility, while the other creates a binding obligation.

2. Is lease to own a good idea?

A lease to own agreement can be a good option if you need time to improve your credit or save for a down payment. It gives you flexibility and time to prepare. However, you may lose the option fee or rent credits if you do not buy, so always review the terms carefully.

3. Do lease-to-own agreements include rent credits?

Many lease to own agreements include rent credits, where a part of your monthly rent goes toward the purchase price. However, this is not guaranteed. You should always check how much is credited and whether those credits are refundable.

4. What happens if I don’t buy the home in a lease purchase agreement?

In a lease purchase agreement, you are expected to buy the property. If you do not complete the purchase, you may lose your upfront payments, rent credits, and could face legal consequences. This is why it is considered a higher-risk option.

5. Can I back out of a lease-to-own agreement?

Yes, you can leave a lease to own contract at the end of the lease. There is no legal obligation to buy. However, you will likely lose the option fee and any rent credits you have built.

6. Which is more flexible between lease-to-own and lease purchase?

A lease to own agreement is more flexible because it gives you a choice to buy or not. A lease purchase agreement is less flexible since it requires you to complete the purchase once the lease ends.

7. Do I need good credit for lease-to-own?

You do not always need strong credit for a lease to own agreement. Many buyers use this option to improve their credit before applying for a mortgage. Still, some sellers may check your financial background before approving the deal.

Authors