Log in

Log in Free Trial

Free Trial karina

karina  4954 views

4954 views  7

7

Handling rental income sounds simple until you’re managing money for multiple owners, properties, vendors, deposits, and maintenance expenses all at once. That’s usually the moment property managers realize spreadsheets and one bank account are not enough anymore. A missed entry, delayed deposit, or mixed transaction can quickly create accounting problems nobody wants to explain later.

That’s where trust accounting for property management becomes essential. It helps property managers separate client funds properly, maintain cleaner financial records, and stay compliant with industry rules and fiduciary responsibilities. More importantly, it creates transparency for property owners who want clear answers about where their money is going.

This guide explains how trust accounting works, why it matters, common challenges property managers face, and how software tools can simplify tracking, reporting, reconciliations, and owner statements.

TL;DR: What You Need to Know

- Trust accounting keeps owner funds separate from business operating money.

- Proper trust accounting helps property managers stay legally compliant.

- Accurate records reduce disputes, confusion, and audit risks.

- Trust accounts simplify owner reporting and monthly statements.

- Rent rolls and trust accounts work together for better financial tracking.

- Property management software helps automate reconciliation and reporting tasks

👉 Simplify your trust accounting and financial management with our comprehensive software. From multiple accounts to detailed reporting, we’ve got you covered. Try RentPost free trial for 30 days.

What Exactly is Trust Accounting For Property Management?

Trust accounting in property management refers to the process of managing and recording financial transactions related to rental properties on behalf of property owners or landlords. It involves the proper handling and documentation of funds received from tenants, such as rent payments, security deposits, and other fees.

Trust accounting basically means having separate accounts for each property in one single banking account. Think of a trust account like a room full of safety deposit boxes. While your banking account holds all of the accounts, or ‘safety deposit boxes’, it allows you to go through and maintain them all individually. No need to worry about funds commingling with that of other property owners or even with your own operating capital and expenses.

Why Use Trust Accounting in Property Management?

Aside from keeping your accounts from commingling, using a trust account allows you to keep diligent track of each property in the instance your company is audited. This also gives you far better and accurate account transactions if you need to pinpoint a specific piece of information.

Let’s look into the key purposes of trust accounting in property management.

1. Safeguarding Client Funds

Property managers often handle rental income, security deposits, maintenance funds, and other financial assets that belong to property owners or tenants.

Trust accounting ensures that these funds are kept separate from the property manager’s personal or business accounts, reducing the risk of misappropriation.

2. Legal and Regulatory Compliance

There are specific regulations and laws in place to protect clients’ funds in property management. For starters, Article 8 of the National Association of Realtors (NAR) Code of Ethics requires property managers to maintain trust accounts for their clients.

According to industry standards and regulations, property managers should also deposit any funds collected on behalf of their clients into the designated trust account in a timely manner, generally within 3-5 business days upon receipt.

Software like RentPost™, can help property managers meet these deposit requirements with online rental payments, like RentPost™’s Payshift payments.

By rapidly depositing monies meant for their clients into properly tracked trust accounts, property managers demonstrate accountability, transparency, and protection of their client’s assets per fiduciary duty.

3. Transparency and Accountability

Trust accounting provides a clear and transparent financial trail, allowing property owners to verify the handling of their funds. It helps build trust between property managers and clients by demonstrating a commitment to financial integrity and accountability.

4. Accurate Record Keeping

Property managers deal with numerous financial transactions, including rent collection, bill payments, and maintenance expenses. Trust accounting ensures accurate and detailed records of these transactions, making it easier to track income and expenses, generate reports, and reconcile accounts.

5. Auditing and Dispute Resolution

Trust accounting systems facilitate audits and help resolve any financial disputes that may arise between property managers, property owners, or tenants. With well-maintained financial records, it becomes easier to identify discrepancies, reconcile accounts, and resolve any discrepancies or misunderstandings.

Overall, trust accounting plays a crucial role in maintaining the financial health and reputation of property management companies by ensuring responsible management of client funds, compliance with regulations, and fostering transparency and trust with property owners and tenants.

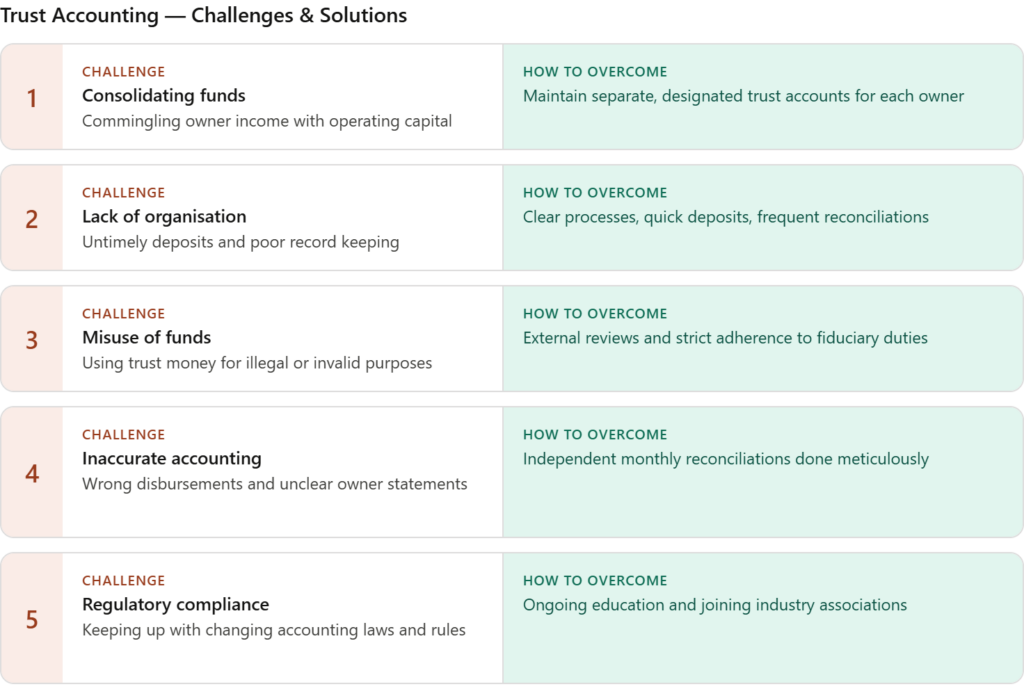

Challenges in Trust Accounting for Property Management

Trust accounting represents a central pillar of the property management business, yet conducting precise, ethical tracking of multiple owner proceeds requiring fast turnarounds exposes firms to heightened liability.

Some of the main challenges of trust accounting in property management include:

- Consolidating funds: Commingling of owner income with operation capital.

How to overcome: Have separate, designated trust accounts for each owner. - Lack of organization: Untimely deposits, poor record keeping of statements.

How to overcome: Develop clear processes, make deposits quickly, reconcile often. - Misuse of funds: Using trust money for illegal or invalid purposes.

How to overcome: Conduct external reviews, follow all fiduciary duties. - Inaccurate accounting: Disbursing wrong amounts to owners, unclear statements.

How to overcome: Perform meticulous monthly reconciliations independently. - Regulatory compliance: Keeping up with changing accounting laws and rules.

How to overcome: Seek ongoing education, join industry associations to stay current.

In an environment demanding impeccable attention to detail regarding other people’s money, property management firms must implement bulletproof systems and oversight to maintain place as an industry bedrock for client trust.

Generating Owner’s Statements from Trust Accounts

Owner’s statements are a rather big part of the accounting side of property management. Each property owner should receive a statement every month giving them a detailed account of their property’s financial standings. These statements include rent and/or utilities paid in by the tenants, service or maintenance payouts, management service fees, and how much actual money is left in their accounts for the property.

Generating an owner’s statement from a trust account in property management involves summarizing the financial transactions and providing an overview of income and expenses related to the property owner’s investments. However, keeping track of all of these transactions can take up a decent amount of time and requires far more organization than just receipts and statements in a shoe box.

The RentPost™ software includes features for generating owner’s statements when linked to trust accounts. This can streamline the process and automate calculations based on the data entered into the system, ensuring accuracy, efficiency, and professional presentation.

Trust Accounts and Rent Rolls

A rent roll is a document that provides a comprehensive summary of rental income generated by a property. It typically includes details about each individual unit or tenant within a property, as well as the lease terms, rental rates, and other pertinent information.

Why rent rolls are important

The rent roll serves as a crucial tool for property owners, real estate investors, and property managers when it comes to income analysis, property valuation, and portfolio management. By analyzing the rent roll, they can determine the following:

- total rental income

- vacancy rates

- lease expirations

- rental growth

Potential buyers and lenders often rely on rent rolls to assess the income-generating potential of properties. Below are the key reasons why property managers should maintain rent rolls:

- Have a consolidated view of occupancy rates, projected collections, tenant rosters and lease terms in a single report

- Assess demand when performing market value or income property analysis

- Better tenant tracking and cash flow visibility for proactive management

- Budgeting and staffing requirements planning

- Accounting and maintenance operations

Individual property trust accounts provide accurate rent rolls at any given time. While a rent roll and a trust account are two distinct components of property management serving different purposes, it is clear how one works for the benefit of the other to simplify the entire rent or property management process.

How RentPost™ helps you in trust accounting for property management

Here are key ways our RentPost™ property management software aids with trust accounting:

1: Automated recording of tenant charges and payments per owner or property

By seamlessly syncing tenant ledgers, payment receipts and profit & loss reports within consolidated, cloud-based software platforms, manual allocation confusion is eliminated. Robust rent collection automation also provides the necessary checks and balances to support growth without jeopardizing fiduciary obligations.

2: Separate accounting for security deposits versus rental income

Properly segregating security deposits into distinct trust accounts shields rental proceeds from improper use before disbursement, while still earning interest if required by state laws. This separation also enables easy deposit refund processing at lease end based on documented move-in versus move-out unit condition reports.

3: Integrated bank account reconciliation and reporting

By syncing external bank data feeds with internal tenant and property financial records, RentPost™ can automatically reconcile balances, alert to discrepancies, and generate more timely oversight reporting. This automation provides quicker visibility into cash flows and trustee performance across managed assets using a unified dashboard.

4: Automatic rent collection reminders and late fee assignment

Automating reminders for upcoming rental payments and tracking overdue accounts for established late penalties reduces administrative tasks while applying policies consistently. This way, staff save time and minimize confusion by letting the technology handle much of the rent collection follow-up process.

5: Electronic monthly statements detailing all transactions

Digitizing monthly statements allows property management firms to efficiently compile volumes of granular transaction data into user-friendly owner reports showing balances, activities and trailing reconciliations. This streamlines communications while enhancing transparency around how proceeds are handled on owners’ behalf.

6: Improved auditing and compliance oversight on multiple levels

Robust property management systems allow customized access permissions so owners can audit transactions or compliance metrics on demand while controlling sensitive data, with detailed activity logging for external examinations. This empowers broader governance through increased visibility despite rapid firm expansion.

7: Real-time unit/tenant statistics

By compiling dynamic occupancy rates, turnover metrics, delinquency ratios, and tenant demographic data across properties into consolidated analytics, owners and managers can pinpoint opportunities for operational improvements or portfolio strategy changes. This provides key performance visibility enabling fact-based decision-making for assets under management.

8: Increased transparency through digitized paper trails

By centralizing the documentation of leases, invoices, statements and inspection photos within a secure and accessible platform, owners gain on-demand visibility. This round-the-clock accountability builds owner trust and confidence despite geographical distance.

FAQs

1. What is trust accounting in property management?

Trust accounting is the process of managing rental income, security deposits, and owner funds separately from a property management company’s operating money. It helps property managers track financial transactions accurately while protecting client funds and maintaining transparency for property owners and tenants.

2. Why is trust accounting important for property managers?

Trust accounting helps prevent commingling funds, improves financial organization, and supports legal compliance. It also creates clear records for audits, owner statements, and dispute resolution. Without proper trust accounting, property managers can face financial confusion, compliance issues, or even legal penalties.

3. Can property managers keep all owner funds in one account?

Property managers generally use trust accounts to separate client funds from business funds. Depending on state laws and company structure, funds may still be tracked separately within the same trust banking system. The key requirement is maintaining accurate records for each owner and property.

4. What happens if trust accounting records are inaccurate?

Inaccurate records can create serious problems, including owner disputes, failed audits, incorrect payouts, compliance violations, and damaged client trust. Even small accounting errors can become difficult to untangle later, especially when multiple properties and transactions are involved.

5. What is included in an owner statement?

Owner statements usually include rent collected, maintenance expenses, management fees, utilities, vendor payments, deposits, and the remaining account balance. These reports help property owners understand exactly how their property is performing financially each month.

6. How does software help with trust accounting?

Property management software automates tasks like rent tracking, reconciliation, owner reporting, payment reminders, and transaction recording. This reduces manual errors, improves organization, and makes handling multiple trust accounts much easier, especially as the number of managed properties grows.

Authors