Log in

Log in Free Trial

Free Trial oojacoboo

oojacoboo  Updated on July 27, 2026

Updated on July 27, 2026  94 views

94 views  0

0

Buying a home can feel close enough to picture but still far away to afford. You may have enough income to handle a monthly payment, but not enough cash for a down payment, closing costs, or a credit profile that makes a lender say yes. That is why rent to own gets so much attention. It sounds like a bridge between renting now and buying later.

Sometimes, that bridge is real. Sometimes, it is expensive, one sided, and full of traps. A good rent to own deal can give you time to save, improve your credit, and lock in a home you truly want. A bad one can leave you with higher rent, repair bills, lost fees, and no house at the end. This guide explains what rent to own is, how rent to own works, and how to tell the difference.

Key Takeaways

- Rent to own is a hybrid agreement that lets you rent a home now and buy it later if certain terms are met.

- The biggest distinction is between a lease option, where buying is optional, and a lease purchase, where buying is usually required.

- Before signing, you should treat the deal like a real home purchase by ordering an appraisal, inspection, and title search, and by having a local real estate attorney review the contract.

- The biggest risks are losing upfront fees, taking on repair costs too early, finding hidden title or foreclosure issues, and reaching the end of the lease without mortgage approval.

- Before choosing rent to own, compare it against FHA, VA, USDA, down payment assistance, and seller financing options.

What Is Rent To Own?

Rent to own is an agreement where you rent a property for a set period and get the right, or sometimes the obligation, to buy it later.

In short, you move in as a tenant first, but the contract also lays out a future purchase plan. That is why people searching what is rent to own and how does rent to own work are often trying to solve the same problem: they want to buy a house, but they are not fully mortgage ready yet.

In many cases, the contract includes an upfront option payment and monthly rent that may be higher than standard market rent. Some deals credit part of that extra money toward the future purchase. Others do not. That is why the contract language matters so much.

Why Buyers Consider Rent To Own

People usually look at rent to own when they are close to buying but not quite there yet.

Common reasons include:

- Need more time to improve credit

- Need more time to save for a down payment

- Want to lock in a home before prices rise

- Need a short runway before qualifying for a mortgage

- Want to test the home or neighborhood before committing

This demand makes sense in a market where affordability remains tight. The U.S. homeownership rate was 65.3% in the first quarter of 2026, while Freddie Mac reported the average 30 year fixed mortgage rate at 6.43% as of July 2, 2026. NAR also reported that first time buyers made up 32% of all home buyers, showing that many households are still trying to break into ownership despite higher borrowing costs.

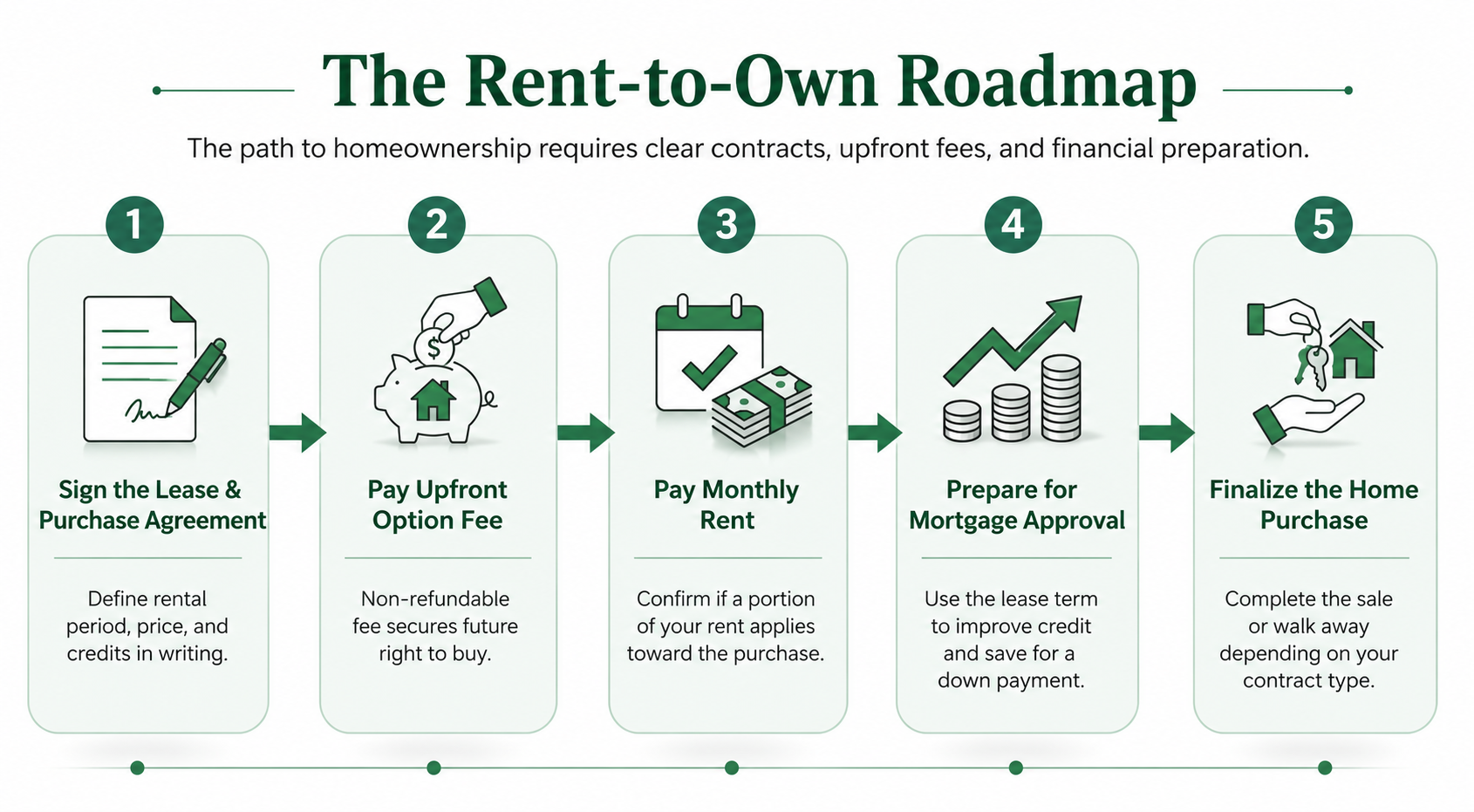

How Does Rent to Own Work Step by Step?

The rent to own process follows a series of simple steps that take you from renting a home to potentially becoming its owner.

Here is a quick overview of how does rent to own work:

- Find a home and agree on the terms.

- Sign the lease and purchase agreement.

- Pay the upfront option fee.

- Make monthly rent payments.

- Prepare for mortgage approval.

- Complete the home purchase or end the agreement.

Let us understand how each step works.

1. The Buyer And Seller Agree On A Home

First, you and the seller identify a property and decide whether the deal will be a lease option or lease purchase.

This is the moment to slow down. A rent to own deal is not just a rental. It is a rental plus a future home purchase, which means you should evaluate the property with a buyer mindset from day one.

2. You Sign A Lease Plus A Purchase Agreement

Next, the contract sets the lease term, future purchase terms, and what happens to upfront fees and rent credits.

Nolo recommends treating the agreement like a real home purchase and making sure the contract clearly states the rental period, purchase price, whether rent credits apply, how financing will work, and who pays closing costs.

3. You Pay An Upfront Option Fee

Many rent to own agreements require money upfront to secure your right to buy later.

This fee is often separate from your security deposit and is commonly at risk if you walk away or fail to qualify at the end. That is one reason the FTC warns that buyers can lose money even in deals that seem legitimate.

4. You Pay Rent During The Lease Term

During the lease, you live in the home like any other tenant, but your payments may not work like a standard rental.

Some contracts apply a portion of rent toward the future purchase. Some simply charge above market rent without meaningful credits. You need exact numbers in writing, not verbal promises.

5. You Prepare For Mortgage Approval

This is the part too many articles gloss over, but it is the part that decides whether the deal succeeds.

During the lease term, you should be improving credit, reducing debt, saving cash, and documenting income. Freddie Mac says buyers typically need at least 3% down, generally 5% to 20%, plus closing costs that often run 2% to 5% of the purchase price. If your contract ends before you are truly loan ready, you could lose the home and the money you already put in.

6. You Complete The Purchase Or Walk Away

At the end of the term, the outcome depends on the contract type.

With a lease option, you usually can choose not to buy, though you may lose fees and credits. With a lease purchase, walking away can trigger legal and financial consequences because the contract may require you to buy.

Lease Option Vs Lease Purchase

This is the most important distinction in the whole article, because many buyers use the two terms as if they mean the same thing.

| Feature | Lease Option | Lease Purchase |

|---|---|---|

| Right to buy | Optional | Usually required |

| Flexibility | Higher | Lower |

| Risk if you do not buy | Usually lose fees or credits | May face financial or legal liability |

| Best for | Buyers still building credit or savings | Buyers who are highly confident they will close |

| Buyer pressure level | Moderate | High |

If your readers want a deeper breakdown, this internal guide on lease to own vs lease purchase is a natural supporting link.

Which One Is Safer

For most buyers, the safer structure is a lease option.

That does not mean it is automatically safe. It only means the legal downside is usually lower if life changes, financing falls through, or the home no longer feels like the right fit. A lease purchase can make sense, but usually only when the buyer is very close to mortgage ready and the legal terms have been reviewed carefully by counsel.

What You Pay In A Rent To Own Deal

A lot of confusion around rent to own comes from the money side, so this section should make the economics clear.

Most buyers will see some mix of four cost buckets.

| Cost Category | What It Usually Covers | What To Watch Closely |

|---|---|---|

| Option fee | Pays for the right to buy later | Whether it is refundable and when |

| Monthly rent | Standard occupancy payment | Whether rent is above market |

| Rent credit | Amount that may count toward purchase | Exact formula and conditions |

| Repair and maintenance costs | Day-to-day or major home issues | Who pays before closing |

Pros And Cons Of Rent To Own

Now that the mechanics are clear, here is the practical tradeoff.

Pros

A good rent to own agreement can help buyers who are not mortgage ready today but expect to be ready soon.

- More time to improve credit

- More time to save cash

- Ability to lock in a home before shopping again

- Chance to live in the property before buying

- Possible rent credits toward the purchase

Cons

The downside is that a weak contract can shift too much risk to the buyer.

- Upfront money may be lost

- Rent may be higher than market

- Repairs may become your problem before you own the home

- You may overpay if the agreed price is too high

- You can still fail to qualify for a mortgage later

- Some deals are scams or hide title, tax, or foreclosure problems

Also Read: Is Rent to Own a Good Idea? Pros, Cons, and Who It’s Really For

Red Flags And Due Diligence Checklist

This is where your article can be more useful than the competitor pages, because this is the section readers actually need before they sign. Use this checklist before you hand over money.

Verify The Seller And The Property

Do not rely on a listing, a handshake, or a friendly story.

The FTC warns that some supposed sellers do not actually own the home, while others have unpaid taxes or foreclosure issues. Run the basic checks first

Due diligence checklist:

- Confirm legal ownership

- Run a title search

- Check for liens or foreclosure risk

- Verify property taxes are current

- Confirm insurance status

- Review HOA status if applicable

Treat The Home Like A Purchase, Not A Rental

You should not skip buyer due diligence just because the purchase happens later.

Nolo recommends ordering an appraisal, getting a professional inspection, and reviewing state disclosure rules before you sign. HUD also recommends counseling, home shopping checklists, and a home inspection as part of a sound buying process.

Property checklist:

- Get an appraisal

- Order a full home inspection

- Review required disclosures

- Estimate near term repair costs

- Check neighborhood comps

- Confirm the agreed price is reasonable

Review These Contract Clauses Carefully

A rent to own contract should answer every money and timing question clearly.

If it does not, do not sign it yet.

Clause checklist:

- Purchase price or pricing formula

- Lease length and purchase deadline

- Option fee treatment

- Rent credit formula

- Late payment consequences

- Repair responsibilities

- Closing cost allocation

- Financing expectations

- Default and termination rules

- Whether the deal is optional or mandatory

This is also a natural place to link internally to seller financing vs rent-to-own, because many buyers compare those paths without understanding that seller financing transfers ownership much earlier.

Get Professional Help Before Signing

This is not overkill. It is basic protection.

HUD recommends talking with a housing counselor, and Nolo recommends having a local real estate attorney review the agreement before signing because rent to own contracts combine lease terms and purchase terms in one complex document.

Alternatives To Rent To Own

A strong article should not assume rent to own is the answer. It should help readers compare it to better options too.

In many cases, a buyer can reach homeownership faster and with less risk through standard financing plus assistance programs.

Options Worth Comparing First

| Option | Best For | Main Benefit | Main Limitation |

|---|---|---|---|

| FHA loan | Buyers with limited cash | Lower down payment path | Mortgage insurance costs |

| VA loan | Eligible service members and veterans | May allow no down payment | Eligibility required |

| USDA loan | Eligible rural buyers | Low or no down payment potential | Location and income limits |

| Down payment assistance | First-time and income-qualified buyers | Helps reduce upfront cash burden | Program rules vary |

| Seller financing | Buyers who can negotiate directly with the owner | Ownership can transfer sooner | Terms vary widely |

| Rent to own | Buyers needing short preparation time | Delays purchase while keeping the target home in play | Higher contract risk |

HUD recommends learning about state homebuying programs, FHA options, and speaking with HUD approved counselors before moving forward.

Why This Matters More Than Ever

Affordability is the reason many renters turn to creative financing in the first place.

NAR reported that 11% of all buyers said saving for the down payment was the hardest step in the homebuying process. Its 2024 analysis also found that buyers ages 25 to 34 put down about 5% on median in 2024, while the typical American borrower put down 10.8%. That tells you two things at once: cash is a real barrier, but many buyers still get into homes without putting 20% down

If your readers are still early in the search process, you can also link to how to find the best home to rent as a practical supporting resource while they compare options.

Final Verdict

The best version of this topic does not sell rent to own as a dream. It explains it as a tool.

Rent to own can work when the buyer is close to being ready, the property is worth owning, and the contract is reviewed with real care. It can be especially useful for renters who need a short runway to improve credit, save more cash, or secure financing while staying put in a home they already know.

But it is not a shortcut. It is a high detail agreement with real legal and financial risk. If the seller cannot prove ownership, if the title is messy, if the contract is vague, or if your mortgage plan is still just a hope, walk away. In many cases, FHA, VA, USDA, or local assistance programs are safer and simpler. And if you are managing rental operations, leases, and tenant communication across properties, RentPost and its pricing options are natural calls to action for owners and managers who need a cleaner leasing workflow.

Frequently Asked Questions

Is Rent To Own A Good Idea?

It can be a good idea if you are likely to qualify for a mortgage soon, the property has been inspected, the seller checks out, and the contract clearly protects your money. It is a bad idea when the deal is vague, rushed, or seller verification is weak.

Do You Need Good Credit For Rent To Own?

Usually, you do not need mortgage level credit on day one. But you still need a realistic plan to qualify for financing later, because many deals fail at the finish line when the buyer still cannot get a loan.

Is The Option Fee Refundable?

Sometimes, but often not. The contract must spell this out clearly. Never assume you will get it back.

Who Pays For Repairs In A Rent To Own Deal?

It depends on the contract. Some sellers keep major repair responsibility. Others push more costs to the tenant buyer. This should be clearly defined before signing.

Can You Back Out Of A Rent To Own Agreement?

With a lease option, you usually can back out, but you may lose fees and credits. With a lease purchase, backing out may trigger legal or financial consequences.

Is Rent To Own The Same As Seller Financing?

No. In seller financing, ownership typically transfers much sooner and the payments work more like a mortgage. In rent to own, you remain a tenant first and buy later if the deal moves forward.

Legal Disclaimer

This article is for general informational and educational purposes only and should not be considered legal, financial, tax, or real estate advice. Rent-to-own agreements can vary significantly by state, country, and individual contract terms. Before signing any rent-to-own agreement, consult a qualified real estate attorney, financial advisor, or licensed real estate professional to review the contract and ensure it aligns with your specific circumstances.

Author